Welcome to Part 2 of our Guide to Navigating Medicare Advantage series! In Part 1, we discussed the differences between Original Medicare and Medicare Advantage. You can find our blog on Part C Plan Basics & Coverage if you missed it here. In Part 2 of the series, we will dive into Medicare prescription drug coverage, also known as Part D.

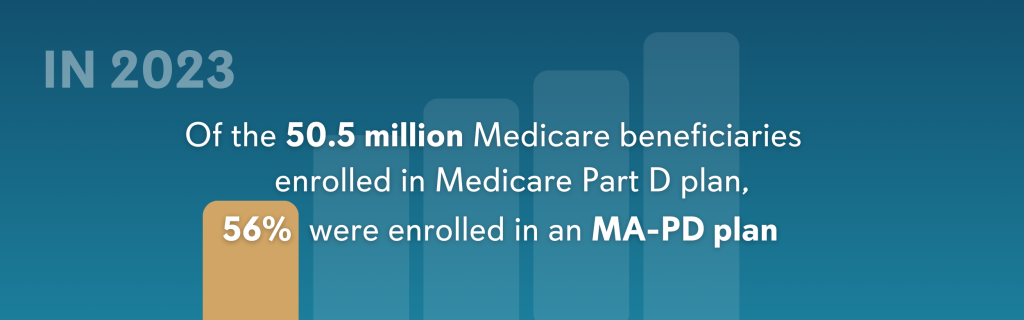

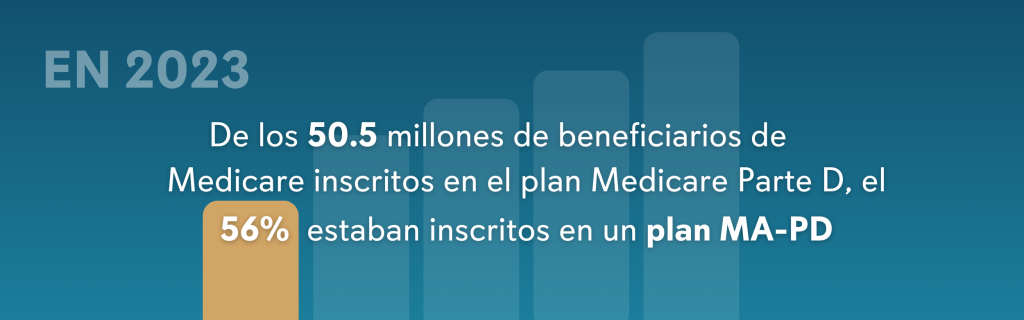

Of the 65 million people covered by Medicare in 2023, more than 50 million were enrolled in a Part D plan[1]. Medicare Part D is a prescription drug benefit offered by private healthcare companies and is designed to help you pay for medications when you become eligible for Medicare. Enrolling in this additional coverage can provide relief from expensive prescription drug costs. However, not all Part D plans are created equal, and knowing what to look for when choosing your coverage is essential.

Part D is Your Drug Plan

Enrolling in a Part D plan is optional, and the prescription drug benefits that come with them are available when you become eligible for Medicare. There are two types of Part D plans:

- A stand-alone prescription drug plan (PDP) enhances your Part A and / or Part B coverage with Original Medicare

- A Medicare Advantage plan with Part D coverage (MA-PD) provides you with a range of benefits in addition to prescription drug coverage.

If you choose NOT to enroll in Part D when you first become eligible for Medicare, you will likely pay a late enrollment penalty if you sign up for a Part D plan later.

Plan Now or Pay Later!

The Part D late enrollment penalty is an additional amount added to your premium for Medicare prescription drug coverage. The penalty is based on how long you go without Part D or creditable prescription drug coverage after your Initial Enrollment Period. You must pay the penalty for as long as you need or use Medicare’s drug benefits.

- The Initial Enrollment Period is your first chance to sign up for Medicare. This 7-month window begins three months before you turn 65, includes your birth month, and ends three months after.

- The Part D penalty is applicable if you are without Medicare drug coverage for 63 or more days in a row.

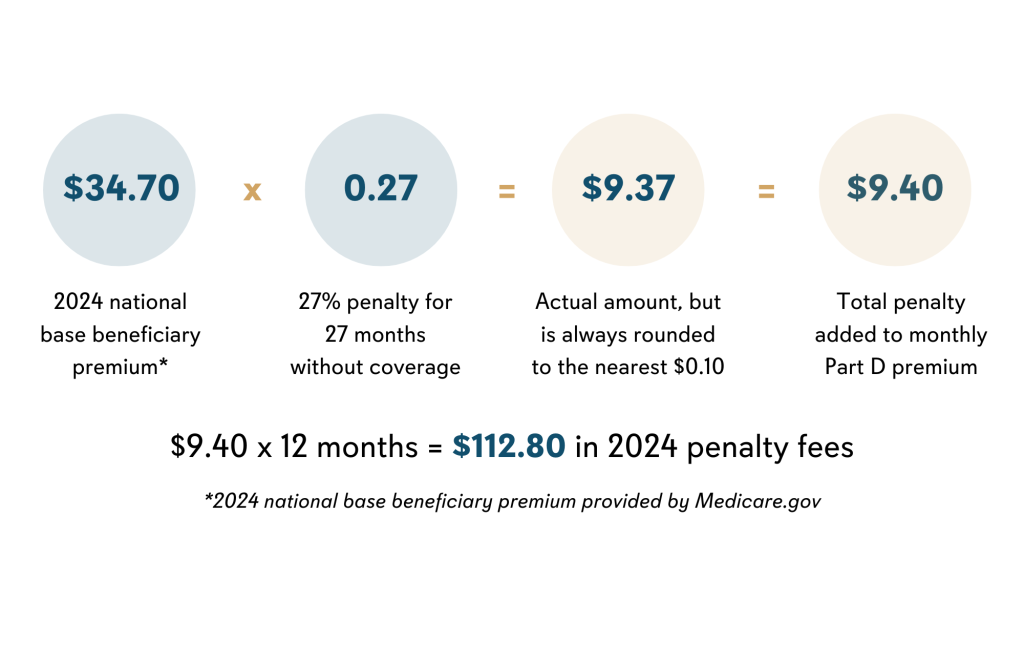

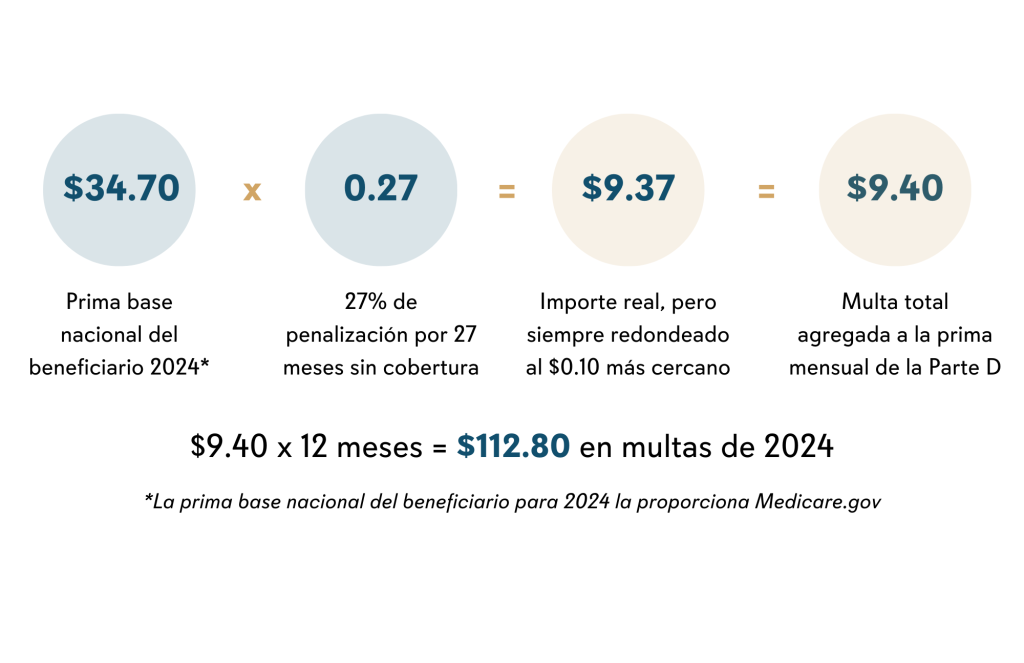

Here’s how the late enrollment penalty is calculated:

1% of the “national base beneficiary premium” ($34.70 in 2024[2]) x the number of full, uncovered months without Part D or other creditable coverage

How it works: Elaine’s Initial Enrollment Period (7-month window mentioned above) ended on September 25, 2021. She did not have prescription drug coverage and decided to join a Part D plan during the Open Enrollment Period that ended on December 7, 2023, for coverage that began on January 1, 2024. For the 27 months without prescription drug coverage (October 2021-December 2023), Elaine is subject to $112.80 in penalties in 2024. Here is how her penalty is calculated:

This penalty doesn’t apply if you receive financial assistance through the Medicare Extra Help program. You can learn more about the Extra Help program below.

Whether you decide on a stand-alone or a Medicare Advantage plan for drug coverage, make sure the specific health plan you’re considering meets your medication needs.

Understanding Part D Coverage

All Part D plans are required to cover a range of prescription drugs. Medicare-contracted insurance companies offering Part D benefits decide:

- What medications their health plans will cover

- How many tiers of medications they will offer

- Which medications fall into which pricing level or tier (this varies by insurance company)

- What coverage they will provide for specific medications and tiers

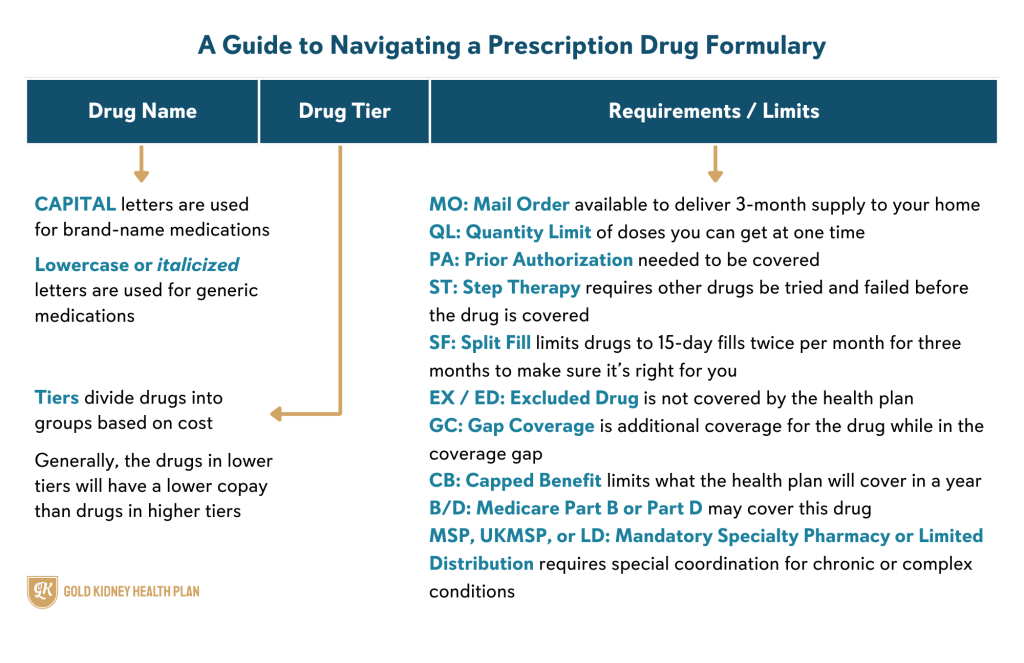

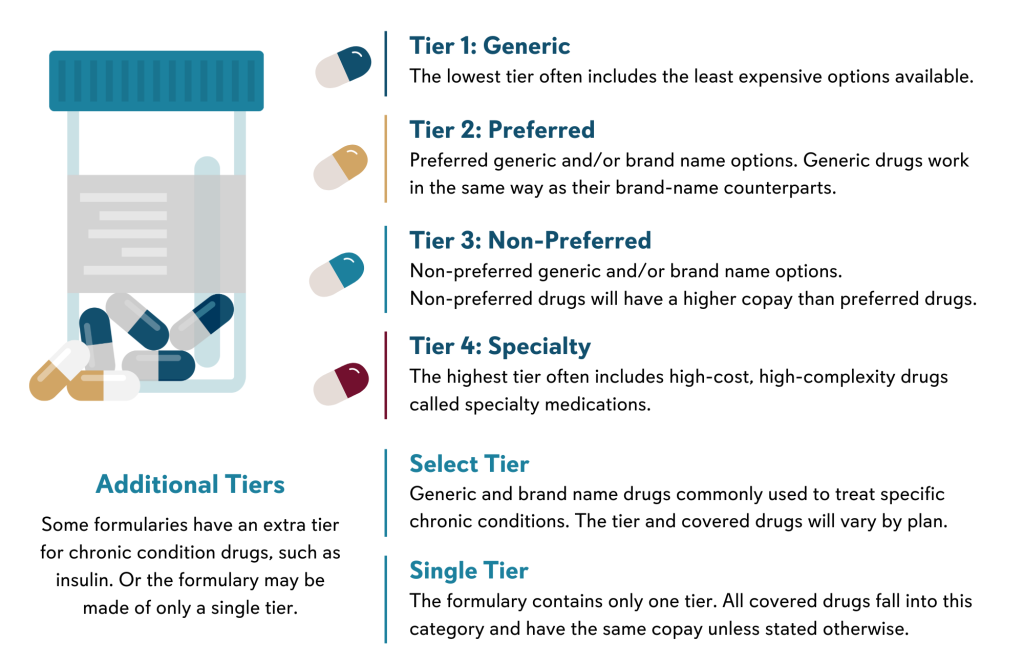

The complete list of generic and brand-name drugs covered by a health plan is called a formulary or a drug list. The formulary is organized into tiers and has different costs for each tier. Generally, the drugs in lower tiers will cost less than drugs in higher tiers. Coverage amounts and specific drugs covered can change at any time, and your health plan must provide you with written notice if you’re taking a medication affected by a drug list change.

To help understand the information found on a plan’s drug list, here are some abbreviations, special rules, and explanations that you should know:

Tiers

The number of tiers and the medications they include varies from plan to plan. Whether you choose Medicare plus a Part D plan or a Medicare Advantage plan with built-in prescription coverage, it’s important to review the formulary and understand what tiers and limitations apply. To get the most from your chosen plan, review coverage for any medications you currently take as well as any medications you might need as you age or develop chronic conditions.

Getting Extra Help with Part D

The payments you make for prescription drugs are considered your true out-of-pocket cost, or “TrOOP.” These are payments made by yourself or payments made on your behalf by individuals or organizations, such as TRICARE, the Indian Health Service, or Medicare’s “Extra Help” program. When you, or those paying on your behalf, have spent a certain amount pre-determined by your health plan, you will enter the catastrophic coverage phase. You will pay little to no cost for drugs in this phase.

Choosing generic medications or using a mail-order pharmacy can help make your medications more affordable. Prescription drugs can still be costly, and if you’re struggling to pay for your medications, there may be programs available to you that can offer financial assistance.

Medicare’s “Extra Help” program is designed to help people with limited income and resources pay for their prescriptions by lowering Part D costs. In some situations, you will get Extra Help automatically, such as if you already receive full Medicaid coverage. If you don’t automatically receive Extra Help, you can apply through Medicare’s website or get help with the application process by contacting your local State Health Insurance Assistance Program.

Beginning in 2025, there will no longer be a coverage gap, also known as the “donut hole” in prescription drug coverage. Instead, the new Medicare Prescription Payment Plan will cap your yearly out-of-pocket costs at $2,000. After your Part D cost have reached this limit, you’ll enter the Catastrophic Coverage Stage, which means you will pay nothing for Part D drugs through the end of the plan year. Medicare’s new payment plan will also give you the option to pay out-of-pocket costs in monthly payments over the plan year.

You can find more information about the Extra Help program, Prescription Payment Plan, and other Part D financial support services through Medicare.gov (click here). And, stay tuned for our upcoming blog where we will share in greater detail what you need to know about the new payment plan program for 2025 and other Part D information!

We hope Part 2 of our Medicare Advantage Guide series has helped you better understand Part D options for prescription drug coverage. If you have questions or would like to learn more about Gold Kidney Medicare Advantage plans and Part D coverage, we would be happy to help. Please contact us at (844) 294-6535 (TTY: 711) or fill out this form and a representative will assist you.

To explore our plans on your own, click your state below:

Stay tuned for more information about Part D!

Y0171_Blog_MedicareABCs2_1124C

Resources:

https://www.medicare.gov/drug-coverage-part-d/how-to-get-prescription-drug-coverage

https://www.medicare.gov/drug-coverage-part-d/what-medicare-part-d-drug-plans-cover

https://kansashealthsystembenefits.com/how-to-read-your-drug-formulary/

[1] https://www.kff.org/medicare/fact-sheet/an-overview-of-the-medicare-part-d-prescription-drug-benefit/

[2] https://www.medicare.gov/drug-coverage-part-d/costs-for-medicare-drug-coverage/part-d-late-enrollment-penalty